What Happens Financially If Income Stops?

For most families, income is the engine that keeps everything moving - the mortgage gets paid, groceries are covered and life ticks along as planned.

But what happens if that income suddenly stops?

It’s not always something we like to think about, but it’s one of the most important financial questions a family can ask.

It’s More Common Than You Think

When people think about risk, they often think about the worst-case scenario.

But in reality, the more likely situations are:

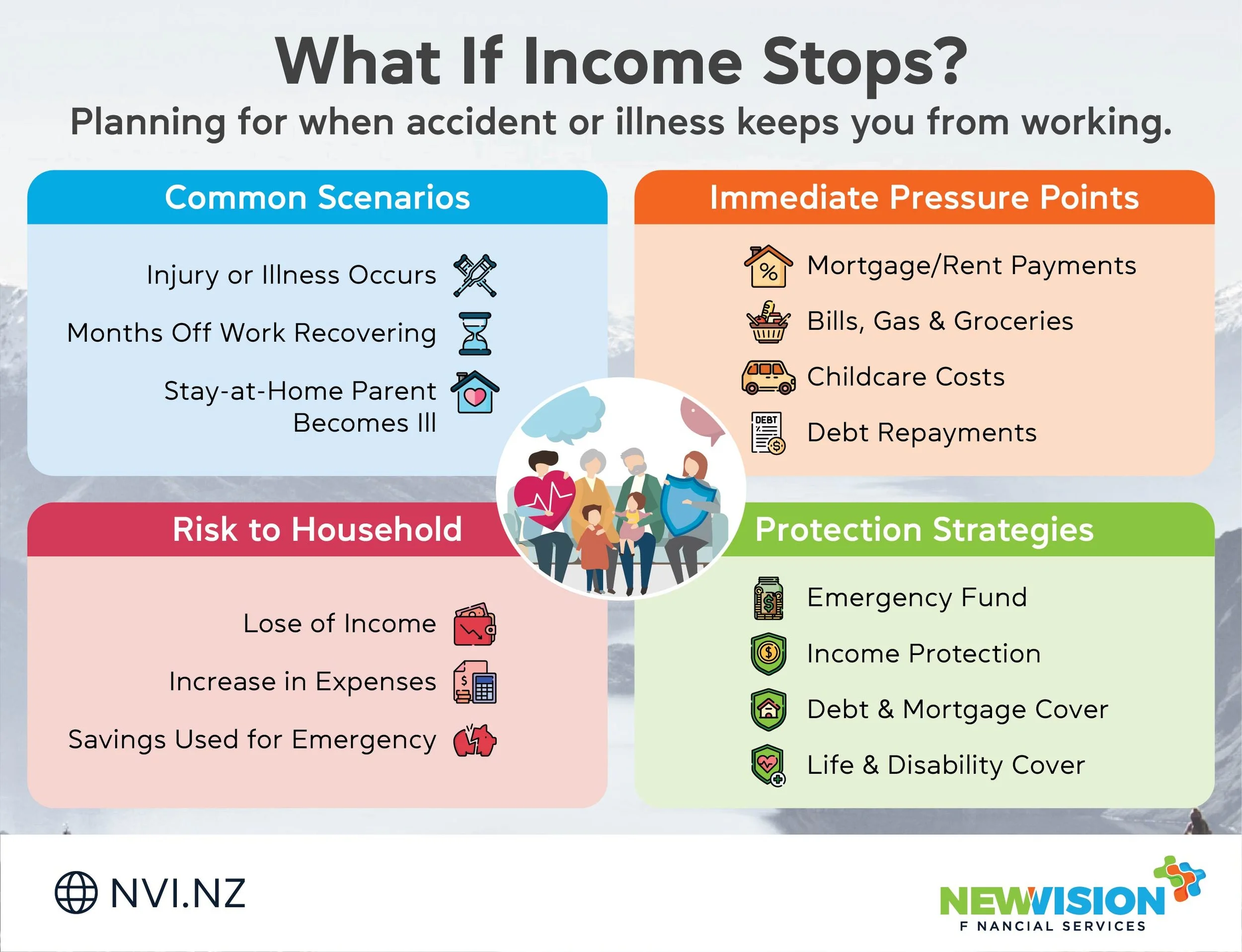

A few months off work due to injury

Time away recovering from illness

Needing to step back for mental health

These aren’t rare events - they’re part of life. The question is whether your finances are set up to handle them.

Where the Pressure Shows Up First

If income slows or stops, the pressure tends to show up quickly - and often all at once.

For most households, that looks like:

Mortgage or rent needing to be paid regardless

Everyday living costs continuing (food, petrol, power)

Childcare or schooling expenses still ongoing

Existing debts not pausing just because income has

Even a short disruption can create stress if there isn’t a plan in place.

The Hidden Risk in Modern Households

Many families today rely on two incomes.

That’s great for lifestyle and flexibility - but it can also create a level of dependency that isn’t always obvious.

If one income stops:

The household may lose its financial buffer

If both incomes are impacted:

The situation can escalate quickly

And one area that’s often overlooked?

Stay-at-home parents.

While they may not bring in income, the role they play has real financial value. If they were unable to manage the household, the cost of replacing that support can be significant.

A Simple Self-Check

It doesn’t need to be complicated. A few honest questions can give you a clear sense of where you stand:

How long could we cover our expenses if income stopped?

Do we have a buffer or are we relying on things continuing as they are?

Would we need to use debt or ask for help?

Have we actually planned for this - or just assumed we’d figure it out?

There’s no judgement in the answers - just clarity.

What Helps Create Financial Resilience

A strong plan isn’t about overcomplicating things. It’s about putting a few key pieces in place so you have options.

That can include:

Emergency savings

A buffer to give you breathing room while you recover or adjust

Income protection

Helping replace income if you’re unable to work due to illness or injury

Mortgage or debt cover

Keeping the roof over your head and reducing financial pressure

Trauma cover

Providing a lump sum during serious health events so you can focus on recovery

Life and disability cover

Protecting your family longer-term if things don’t go to plan

It’s Really About Control

At its core, this isn’t just about insurance or risk.

It’s about control and peace of mind.

Having a plan in place means:

You’re not making rushed decisions under pressure

Your family has stability during uncertain times

You have time to focus on what actually matters - recovery, wellbeing, and each other

A Different Way to Think About It

Instead of asking “What if something happens?”, a better question might be:

“If something did happen - would we be okay?”

If the answer is “I’m not sure”, that’s actually a really good place to start.

Let’s Make It Simple

You don’t need to have everything figured out.

Sometimes a quick conversation is all it takes to:

Understand where you currently sit

Identify any gaps

Put a plan in place that feels manageable and right for your family

If it’s something you’ve been meaning to think about, this is your sign to take that first step.

Nimalka Perera

Business Development Manager

New Vision Financial Services

Plan your future and let us help you have peace of mind along the way.